| |

| |

Challenges Facing the Oil and Gas Sector During Times of Energy Change | |

| Nitin Konde |

As the global community moves toward renewable energy sources, oil and gas industries face a serious problem. Companies' near-term profits are driven by fossil fuels, but their long-term social acceptability and profitability could be jeopardised if they don't respond to rising calls to cut greenhouse gas emissions.

|

What clean energy changes mean for the oil and gas business, and what the industry can do to hasten those transitions, need to be made crystal apparent.

The pressure on all industries to find answers to climate change will only increase regardless of the course the world takes to limit the rise in global temperatures. The recently released report by the IEA, Oil and Gas Industry in Energy Transitions, argues that while some oil and gas companies have taken steps to support efforts to combat climate change, the industry as a whole could play a much more significant role thanks to its engineering capabilities, financial resources, and project-management expertise.

According to Dr. Fatih Birol, Executive Director, International Energy Agency, "no energy industry will be impacted by clean energy transformations." "It's important for everyone in the sector to think about what to do in response. There is no room for inaction.

Because of the unique challenges faced by each oil and gas company, there is no one best strategy for navigating the market.

Dr. Birol has stated that the first order of business for the industry as a whole is to work toward a smaller ecological impact. The extraction and distribution of oil and gas accounts for about 15% of worldwide energy-related greenhouse gas emissions at present. These emissions can be reduced substantially by simple and fast measures.

The single most significant and cost-effective option for the sector to reduce these emissions is to reduce methane leakage to the atmosphere. However, there are also more options to reduce the emissions intensity of delivered oil and gas by doing things like putting an end to routine flaring and incorporating renewables and low-carbon energy into new upstream and LNG facilities.

Dr. Birol elaborated, "Oil and gas companies, with their extensive knowledge and deep pockets, can play a crucial role in accelerating deployment of key renewable options such as offshore wind, while also enabling some key capital-intensive clean energy technologies, such as carbon capture, utilisation, and storage, and hydrogen, to reach maturity." The industry's participation is crucial if these technologies are to reach the critical mass necessary to make a dent in emissions.

There are several oil and gas firms that are branching out into renewables and other low-carbon energy sources. The highest outlays have gone to solar PV and wind, but so far, non-core area investment by oil and gas corporations has averaged roughly 1% of overall capital spending. In addition to increasing their investment in R&D, some oil and gas firms have diversified by acquiring existing non-core businesses, such as those involved in electricity distribution, electric-vehicle charging, and batteries. Nonetheless, there are few indications of the widespread reallocation of capital that is essential to put the globe on a more sustainable course.

Increasing funding for energy sources like hydrogen, biomethane, and advanced biofuels that can replace oil and gas in the energy sector while producing fewer greenhouse gas emissions is a crucial step. If the world is to get back on track to combat climate change, low-carbon fuels would need to account for about 15% of overall expenditure in fuel supply within the next decade. Transitions are made far more difficult and expensive without access to low-carbon fuels.

Dr. Birol argued that in order to tackle the magnitude of the climate crisis, a wide coalition of governments, investors, enterprises, and anybody else who is serious about cutting emissions would be necessary. The oil and gas sector must be fully invested in this initiative, the report says.

With no question, low-carbon electricity will become the dominant force in the global energy mix of the future. Even in rapid transitions to sustainable energy sources, investment in oil and gas projects will be necessary. Stopping all new investment in existing oil and gas fields would result in an annual drop of about 8% in production. This is more than could be explained by a decrease in worldwide demand, therefore new and current fields will continue to get investment.

For as long as oil and gas are in demand and yield satisfactory returns on investment, some business owners may prefer to maintain a focus on these commodities. Companies in this sector will also need to deliberate on how to best respond strategically to emerging threats. National oil corporations have the responsibility of caring for their country's hydrocarbon resources, and their government owners and host societies depend largely on the revenue from oil sales.

More than half of world oil production and an even bigger portion of reserves are controlled by national oil companies. While some function admirably, many are ill-prepared to deal with the new realities of the world's energy markets. Shifts to development models are inevitable in many major resource holders, and these changes have led a number of countries to recommit to reform and diversify their economies. As long as they are running efficiently and keeping an eye out for potential threats and possibilities, national oil firms can be a pillar of economic stability during this transition.

For as long as oil and gas are in demand and yield satisfactory returns on investment, some business owners may prefer to maintain a focus on these commodities. Companies in this sector will also need to deliberate on how to best respond strategically to emerging threats. National oil corporations have the responsibility of caring for their country's hydrocarbon resources, and their government owners and host societies depend largely on the revenue from oil sales.

More than half of world oil production and an even bigger portion of reserves are controlled by national oil companies. While some function admirably, many are ill-prepared to deal with the new realities of the world's energy markets. Shifts to development models are inevitable in many major resource holders, and these changes have led a number of countries to recommit to reform and diversify their economies. As long as they are running efficiently and keeping an eye out for potential threats and possibilities, national oil firms can be a pillar of economic stability during this transition.

|

Oil and gas's major options for coping with the energy transition

Most recently, climate change has emerged as one of the most significant systemic hazards to the global economy. A move away from a hydrocarbon-heavy energy system and toward one dominated by low-carbon sources was already underway long before COVID-19. The recent occurrences have "sharpened investors' interest in sustainable and resilient assets, particularly renewables," according to a research published by the International Renewable Energy Agency. More and more investors are looking for bets that lower their sensitivity to climate change and the danger of stranded assets. Wall Street Journal research indicates that oil and gas firms in North America and Europe wrote down asset values totaling $145 billion, or approximately 10% of their market value, in the first three quarters of 2020. Collectively, the signatories to the Climate Action 100+ programme oversee more than $50 trillion in assets, and their number continues to grow. Environmentally responsible spending is also a cornerstone of many governments' efforts to stimulate the economy. And in a move that is unparalleled anywhere in the world, Denmark has decided to halt all future licencing rounds for the North Sea in preparation for the region's eventual decommissioning of oil and gas production by 2050. Oil and gas firms need to make strategic decisions in light of these dynamics, both to strengthen their financial and public image and to choose if and how to reposition themselves to take advantage of the increasing low-carbon winds of change.

Strengthening the foundation of the company

Since 2000, the average oil and gas company's annual total returns to shareholders (TRS) have underperformed the S&P 500 by seven percentage points. Indications like this show that the status quo business model of the industry has been in jeopardy for some time. According to our findings, the global capital investment by the sector over this time period was more than $10 trillion. Overinvestment in the cyclical economy has made it more difficult to generate a profit.

Historically, the cost position of oil and gas assets, especially those in the upstream and refining sectors, has been used as a measure of financial stability and the potential for outperformance. To a greater extent than ever before, financial resilience is becoming a function of climate resilience as we gain a deeper understanding of the physical risks from a changing climate (that is, the direct and indirect risks to assets from climate-related hazards) and transition risks (such as societal pressure, technological disruption, or shifting consumer preferences). Oil and gas firms have been under scrutiny from investors and experts who are trying to determine the extent to which they contribute to global warming. There is a rising tide of public pressure on the oil industry to standardise the reporting of greenhouse gas emissions from operations and whole value chains. Open Group is one organisation trying to improve technology to digitally track the overall carbon footprint of the oil and gas industry. 8 There are others who would like to see investments put to a broader test of their environmental, social, and governance (ESG) viability.

Oil and gas firms' first line of defence against falling commodity prices and rising carbon prices should be a well-diversified investment portfolio. Beyond the no-regrets decarbonization of their operations and supply chain, CEOs may enhance their positions by taking two crucial measures.

Quality Assets Targeting Promising Hydrocarbon Markets

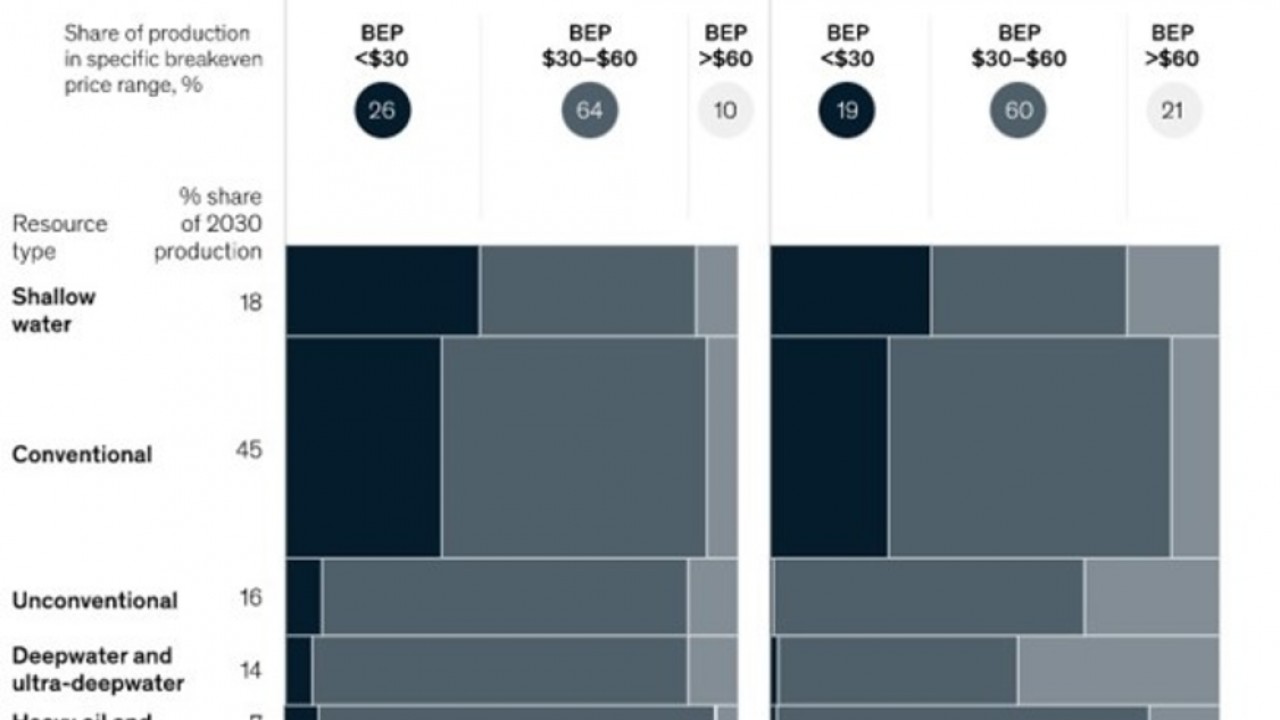

Future investments should be focused on "advantaged" resources, which provide the optimal mix of low break-even pricing and low emissions intensity in order to make a portfolio more financially and climatically resilient. We studied how the global portfolio of upstream oil-focused investment projects fares in terms of competitiveness at varying carbon and commodity prices . Scope 1 and Scope 2 emission estimations from Stanford University's Oil Production Greenhouse gas Emissions Estimator are used in the model. The model takes into account all producing fields and takes the investment choice out of the equation. This dataset provides some straightforward findings, despite the abundance of estimates for emissions and the large variation between them.

Emissions vary greatly from basin to basin and asset to asset, putting an even greater premium on performance. As with carbon-price mitigation through decarbonization activities, the fundamental position of an asset on the cost- or emissions-performance curve can be substantially altered through actions to increase operating efficiency and capital discipline, resulting in lower break-even economics. Opportunities for profitable growth in the hydrocarbon business will diminish without considerable efforts in these areas. Oil and gas firms will need to high-grade their portfolios to access market finance at favourable rates as financial markets demand for greater transparency of the risks and rewards of individual investments under alternative commodity and carbon-price scenarios.

|  |

Identify the hydrocarbon assets that are the least robust and rationalise them

Oil and gas portfolios can enhance their emissions performance and profitability by shutting down their least productive and most carbon intensive wells and associated assets. One North Sea operator found that retiring 20% of its well stock (those with the highest water-cut, lowest hydrocarbon throughput, and highest energy intensity) greatly improved the portfolio's cost efficiency and emissions intensity. A Nigerian upstream firm, for instance, discovered that reinstating each closed-in string did not increase value or decrease emissions during well campaigns despite being the industry standard. In reality, a third of the well chances were able to capture two-thirds of the profits with no net increase in emissions, as shown by the creaming curve, which tested opportunities against value and emissions. Consequently, most oil and gas firms will have no regrets about investing in high-grade physical asset footprints to strengthen the financial and regulatory resilience of current hydrocarbon portfolios.